They’re ugly

This part is real and worth saying out loud. A 500,000 square foot warehouse with no windows, ringed by chain-link fence and humming with industrial cooling, dropped next to your neighborhood, will never be loved. Even the most generous architectural treatment makes it a big gray box. But ugliness alone does not produce the kind of organized resistance we are seeing. Plenty of ugly things get built without protests.

The public pays

States compete for hyperscale projects by handing out sales tax exemptions on the servers themselves, plus property tax abatements, plus discounted power deals. Good Jobs First tracks these and the numbers are not small. Ten states each lose more than $100 million a year to data center carve-outs. Texas and Virginia each forgo around a billion. Virginia’s abatement alone cost public schools an estimated $267 million in fiscal 2024. Amazon’s New Carlisle, Indiana complex was awarded $8.28 billion in incentives, the largest single subsidy package on record.

The standard pitch for these deals is jobs. The reality, by the operators’ own filings, is that a hyperscale campus runs on a few hundred permanent staff. Meta’s $10 billion Lebanon, Indiana site created about 300 permanent jobs. A 500 MW Google campus in Kansas City created 200. Good Jobs First put the math together across eleven large facilities and found the public was paying roughly $2 million per permanent job.

And the profits stay private

The flip side is what those facilities earn. AWS booked $107 billion in revenue in 2024 and roughly $40 billion in operating income, a 37% operating margin. Microsoft’s cloud segment runs above 40%. Combined 2025 capex for Microsoft, Google, Amazon, and Meta sits around $300 billion. 2026 looks closer to $700 billion.

So the trade, baldly: a county forgoes hundreds of millions in taxes and gets a few hundred jobs. The owner of the campus earns billions, in perpetuity, on top of subsidized power. The deal is not subtle.

Almost nobody owns the upside

A common response is that profits flow back to ordinary people through retirement accounts. About 58% of US households own some stock, directly or through 401(k)s and IRAs, and that share is at a record high. The flip side: 42% own no stock at all. For them, the data center economy produces no participation upside whatsoever, only the local costs.

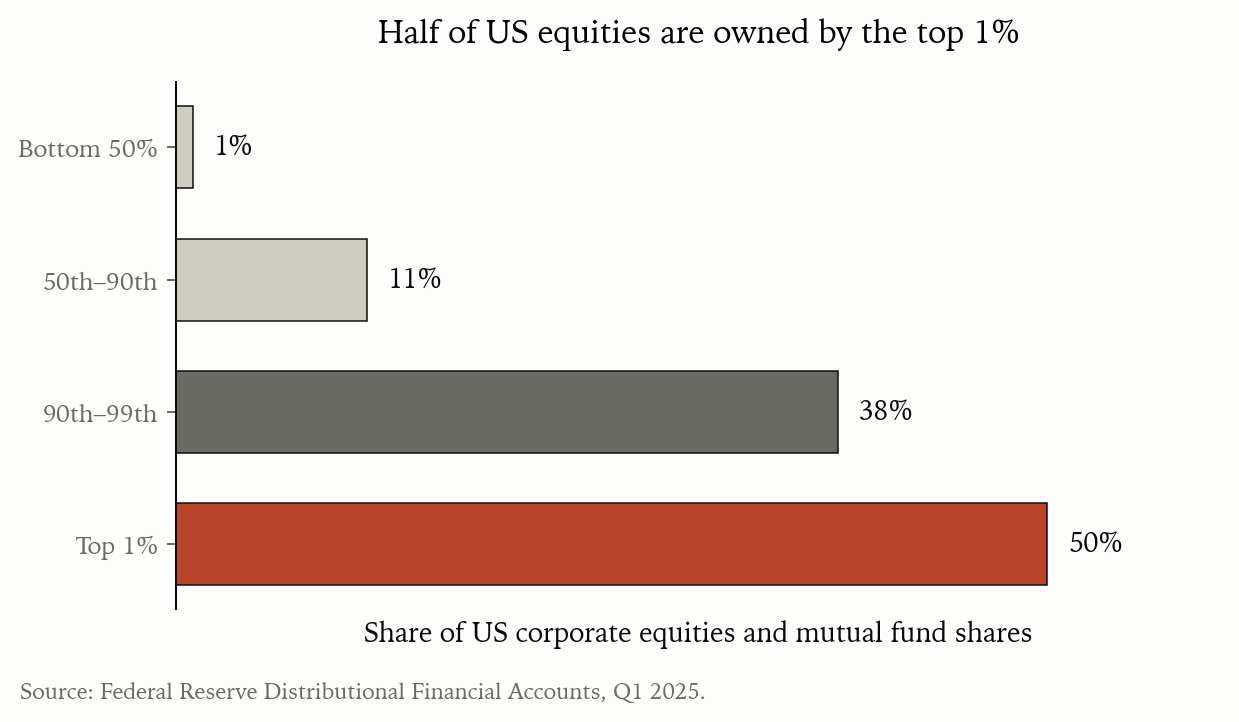

For the households that do participate, the dollar concentration is extreme.

The top 1% of households owns about half of all corporate equity. The top 10% owns roughly 88%. The bottom half owns about 1%. So when AWS books another quarter at 37% margins, the gains accrue almost entirely to a small slice of the country. The median direct stock holding among households that own stock at all is around $15,000. That is a rounding error compared to what a hyperscaler earns in an afternoon.

Inflation makes it worse

For the 42% with no stock, and the much larger share with only a token amount, there is no automatic inflation hedge on savings. Cash in checking and savings accounts erodes directly. Home equity helps if you own a home. Wages can keep pace over long windows but get whipped around during inflation shocks like the one we just lived through.

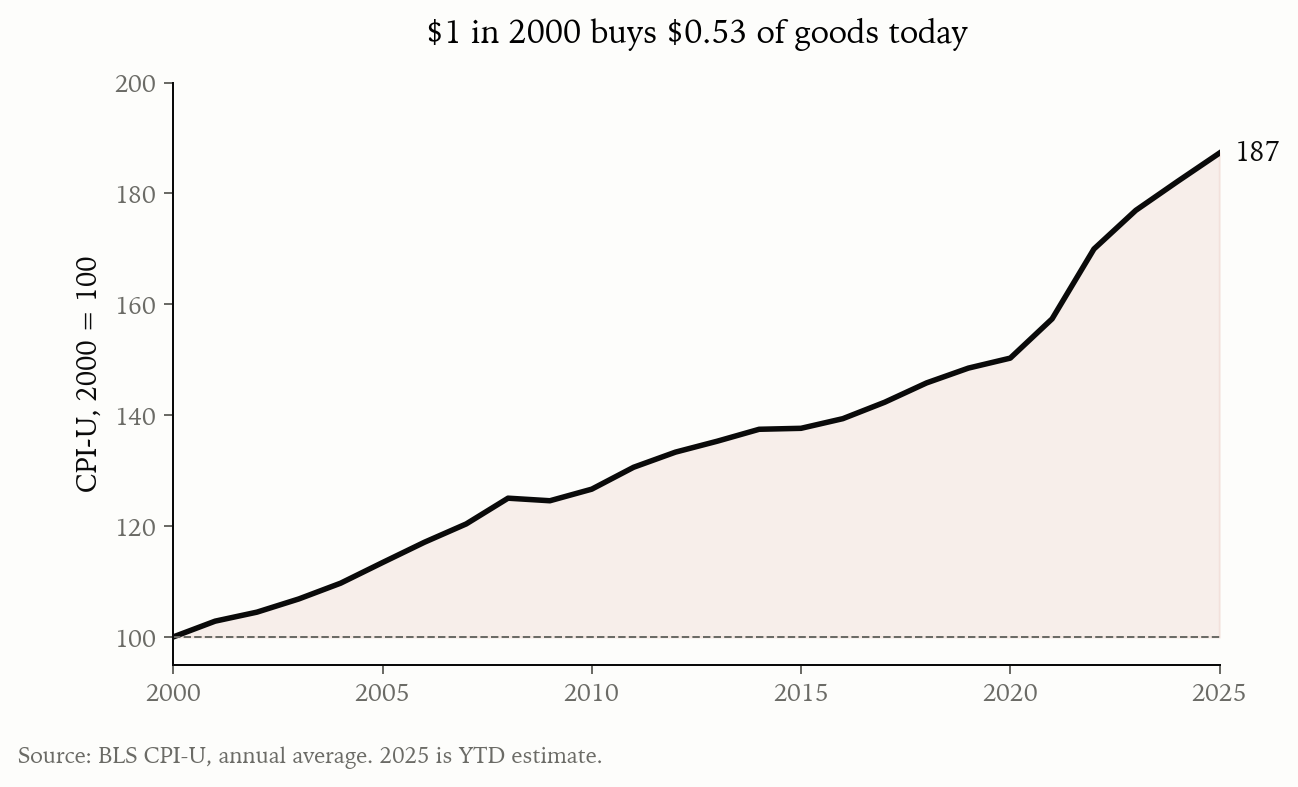

A dollar saved in 2000 buys about 53 cents of goods today. From 2020 alone, prices are up 23%. Households without meaningful equity exposure got smaller in real terms while the data center economy got bigger. The asset that protects against this, broad equity ownership, is exactly the asset most of these households do not have.

Even public market investors are getting cut out

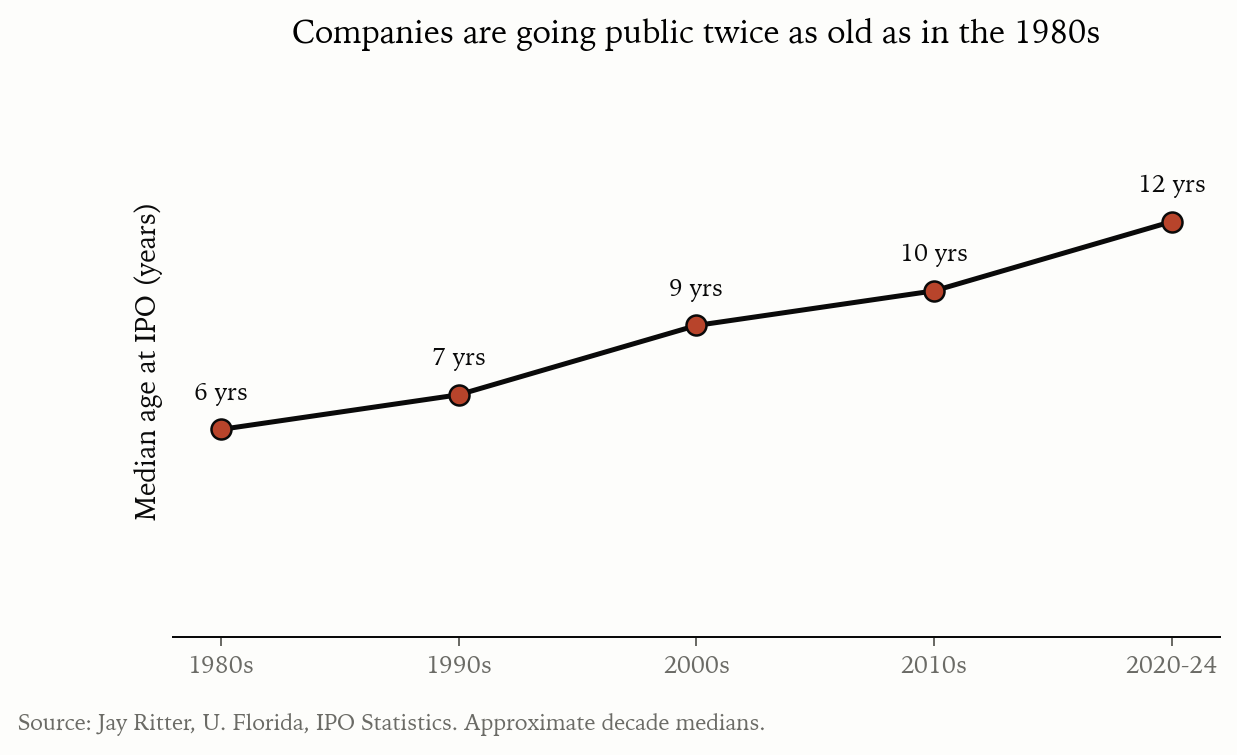

The structural deal for a household that does own equities used to be: companies grow up, go public while there is still a lot of growth ahead, and you buy in through a 401(k) or a broker. That deal is fading.

Companies are going public roughly twice as old as they did in the 1980s. The 1980s median was around six years from founding to IPO. The 2020s are running around twelve, with 2024 IPOs averaging closer to fourteen. The most valuable AI and cloud businesses are not going public at all.

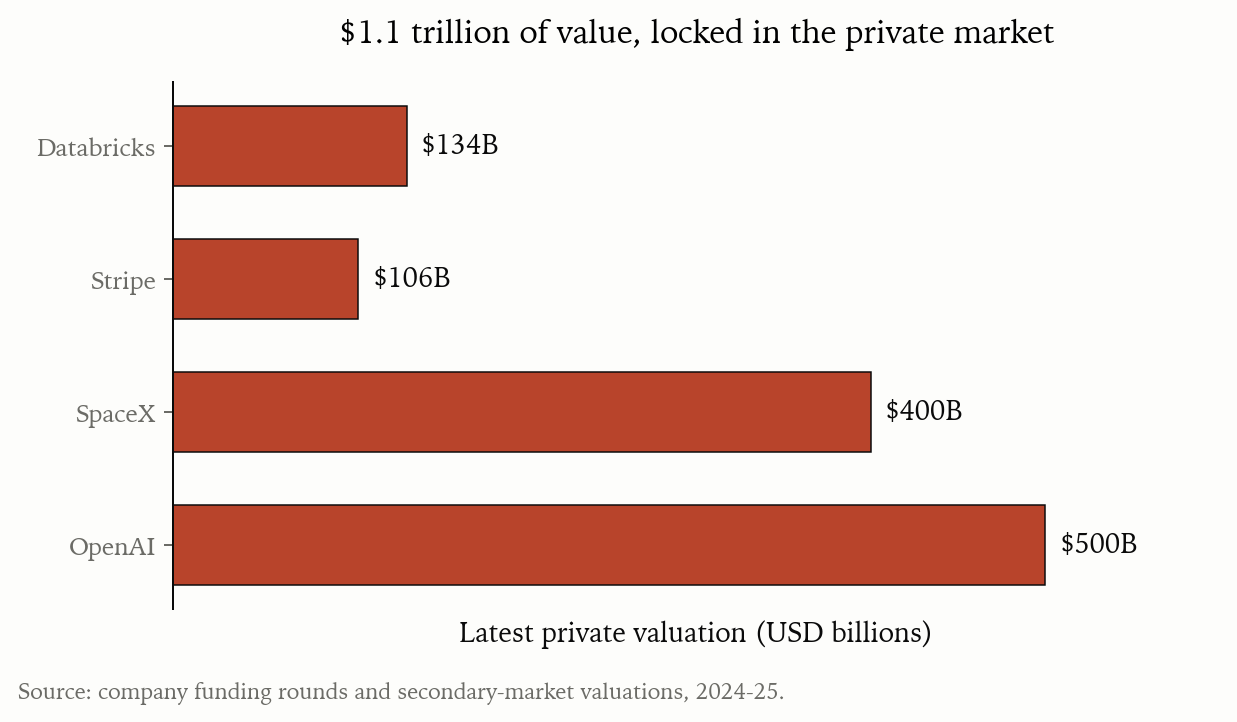

OpenAI is marked at $500 billion in 2025 secondaries. SpaceX is above $400 billion. Stripe is around $106 billion. Databricks just printed $134 billion. These are companies whose products are absolutely central to the data center buildout. A public market investor cannot own a share of any of them. By the time these companies do go public, if they ever do, the highest-multiple years of growth will have already accrued to a few thousand private investors, employees, and funds.

So the picture for an ordinary saver is: cash loses purchasing power, equity ownership is concentrated at the top, and the best new businesses are kept in private hands for a decade longer than they used to be. The data center is the most visible piece of plant for that economy. Of course it draws fire.

The counter-argument

It is worth being honest about what the other side has.

Property tax revenue from data centers, where it survives the abatements, can be very large. Loudoun County, Virginia, the densest data center cluster in the world, reports that data centers occupy about 4% of commercial parcels and produce something like 38% of general fund revenue. The county estimates that residential property taxes would be about $5,800 per household higher per year without that base. That is a real benefit to real people who live in Loudoun.

Data centers are also genuinely critical infrastructure. Cloud, AI, payments, government services, all of it runs on them. We are going to build a lot more of them whether the local politics like it or not.

The dismissal

The public response from people with the largest exposure to the buildout mostly does not engage with any of this. Take Marc Andreessen, whose firm a16z is invested in Databricks, Mistral, Pinecone, xAI, and dozens of other AI companies that all need data center capacity to run. He recently endorsed a thread arguing that the anti-data-center movement is just the latest version of an activist playbook.

The framing collapses the entire complaint into pattern-matching. Anyone objecting must be running someone else’s script. The possibility that a county might do the math on a $2 million per job subsidy and reach an uncomplicated conclusion gets no airtime.

This is the default. When the people most exposed to the upside cannot imagine a substantive reason for the resistance, the resistance will keep happening, and they will keep being surprised by it.

The feeling makes sense

People are right to feel that something is off when a hyperscaler builds a humming concrete block next to their school district, takes a $2 million per job subsidy, and ships the profits to a shareholder base they will never be part of. The aesthetic complaint is the easy one to make at a zoning meeting. The deeper complaint is harder to put into a public comment, but it is the one driving the room.

]]>